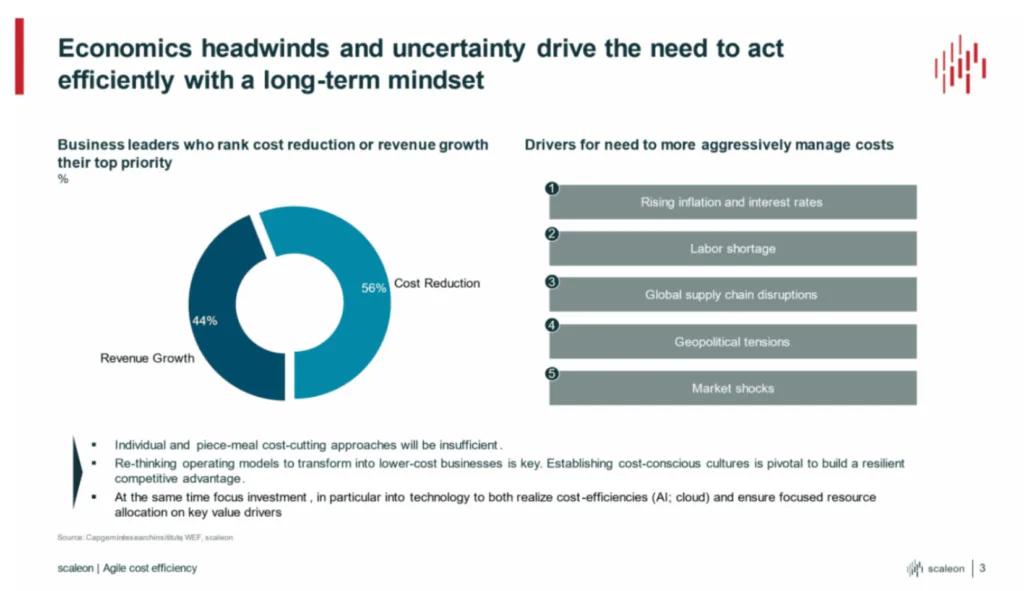

Improving cost efficiency in a lasting way without putting innovation capacity and growth at risk is of great importance for companies today. Rising inflation, interest rate increases, supply bottlenecks, and geopolitical uncertainties make a purely static approach to cost management insufficient. A targeted cost efficiency strategy is essential for remaining competitive over the long term and optimising the EBIT margin.

Rather than short-term cost-cutting measures, what is needed is an approach that combines flexibility with cost control — this is precisely where the concept of agile cost efficiency comes in.

This method combines proven cost optimisation approaches with agile principles in order to enable companies to design their cost structure more efficiently and dynamically. The goal: lasting cost efficiency that not only enables savings but simultaneously strengthens the resilience of the company, improves the EBIT margin, and supports growth. We help you scale your company: Growth strategies with scaleon.

1. Why companies should pay greater attention to cost efficiency

Companies today face unprecedented economic uncertainty. Rising inflation, volatile raw material prices, supply bottlenecks, and geopolitical tensions are placing companies under enormous cost pressure. At the same time, competition is intensifying and the pressure to achieve a sustainable EBIT margin is growing. In this environment, it is no longer sufficient to simply cut costs in the short term — what is required is a long-term, viable cost efficiency strategy.

EBIT margins vary considerably by industry.

EBIT margins vary significantly by industry in Germany. According to an analysis by Gesamtmetall, the return on sales in the metals and electrical industry stood at 2 to 3% in 2022. According to Meyer-Industryresearch, the average EBIT margin of the top 100 companies in German mechanical engineering was 6.7% in 2018. Logistics service providers achieved an average EBIT margin of 3.4%. These differences highlight the need for industry-specific cost efficiency strategies in order to optimise profitability.

Many companies continue to rely on traditional cost management methods that frequently target rigid cost-cutting measures and across-the-board reductions. These approaches often fall short, however: straightforward cost reductions do lead to savings in the short term, but in the long term they impair the competitiveness, innovation capacity, and agility of a company. A purely reactive approach, such as reducing budgets or cutting investments, increases the risk of missing growth opportunities and losing competitive advantage.

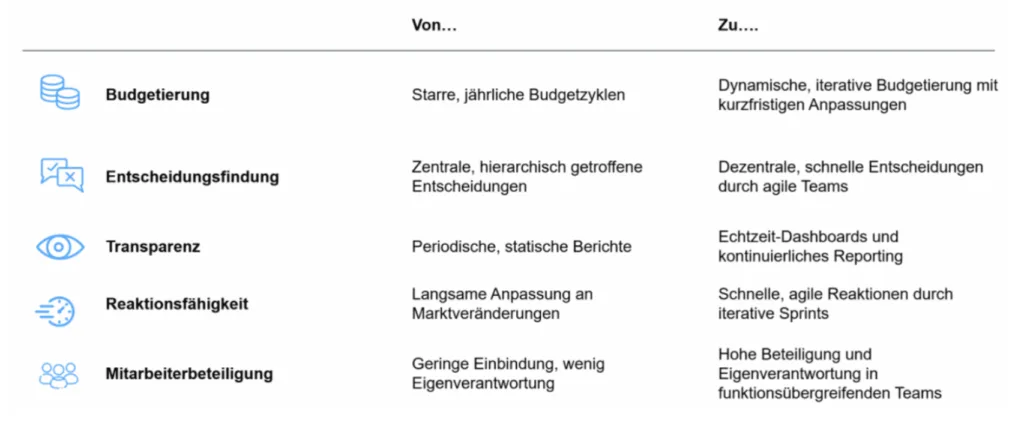

The better approach: agile cost efficiency.

Here is a brief overview of the two methods in comparison.

To remain viable in a volatile market environment, companies need dynamic, agile cost management that combines cost efficiency with strategic investment. This is where the concept of agile cost efficiency comes in: rather than mere cost-cutting measures, it integrates flexible budgeting, iterative optimisation, and data-driven decision-making processes in order to reduce costs over the long term while simultaneously improving the EBIT margin in a lasting way.

The core principles of agile cost efficiency are:

- Dynamic cost control: Rather than fixed budgets, an agile system enables flexible resource allocation that can adapt quickly to market changes.

- Value-driven cost efficiency: Every expenditure is assessed according to its contribution to value creation, making it possible to identify and eliminate unnecessary costs.

- Data-driven decision-making: Through the use of real-time controlling, budgeting tools, and automation solutions, cost reductions can be steered in a targeted manner.

- Iterative optimisation: Agile methods such as sprints and OKRs (Objectives and Key Results) ensure continuous improvement of cost efficiency and prevent inefficient structures from taking hold.

Through this approach, cost efficiency is not treated as a one-time project but embedded as an ongoing, strategic process. Companies that pursue agile cost efficiency can not only realise short-term savings but also optimise their cost structure over the long term, better preparing themselves for future challenges and strengthening their market position.

2. Improving the EBIT margin through agile cost efficiency

In a dynamic market environment, simply cutting costs across the board risks losing innovation capacity and growth potential.

This is where agile cost efficiency comes in: rather than pure cost-cutting, every line of expenditure is assessed for its actual contribution to value creation.

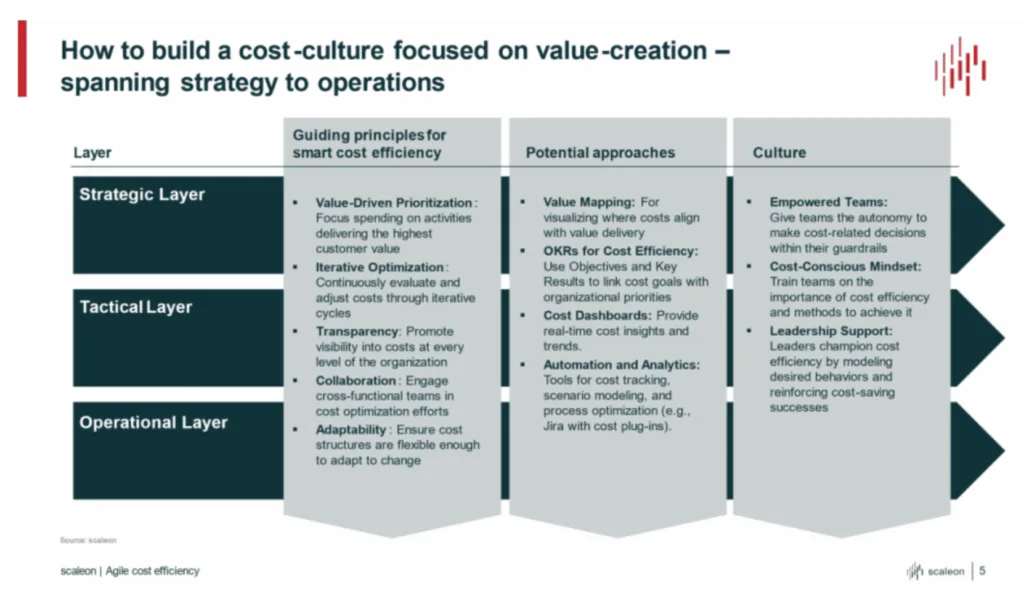

A central approach here is value mapping: cost structures are analysed and assigned to their respective value streams in order to identify precisely which processes deliver genuine customer benefit and which can be eliminated as non-value-adding. Through this data-driven cost control, companies can optimise their financial strategy in a targeted manner and improve their EBIT margin without putting growth or operational performance at risk.

The key principles of value-oriented cost efficiency:

3. Agile cost efficiency: why flexibility in cost management is essential

To make operational processes more efficient, agile methods can enable rapid adaptation to changing market conditions. This allows cost structures to be optimised flexibly without putting long-term growth opportunities at risk.

3.1. Three principles for agile cost management

- Iterative work cycles: Through short, regular sprints, budget optimisation measures are tested, evaluated, and adjusted. This allows savings potential to be identified more quickly and implemented effectively.

- OKRs (Objectives and Key Results): Measurable goals that connect financial governance with corporate priorities. This creates a clear link between strategic planning and operational execution.

- Automated dashboards and real-time reporting: Digital controlling tools enable continuous monitoring of budget and cost structure, allowing companies to make well-founded, data-driven decisions.

This continuous optimisation process makes cost management a dynamic component of corporate strategy.

3.2. From cost management to EBIT optimisation

Modern companies no longer view cost control as a pure savings programme, but as a key to financial stability. Successful organisations embed an agile financial strategy directly into their decision-making processes.

- Flexible budgeting: Rather than rigid annual budgets, resources are allocated dynamically. This allows investments to flow precisely where they create the greatest value for the company and the EBIT margin.

- Operational embedding: Cost-saving measures are not isolated projects but an integral part of day-to-day business. Employees are given the authority to make cost decisions independently and to actively integrate cost awareness into their processes.

- Strategic alignment: Financial efficiency and corporate goals must be synchronised. Through precise coordination between controlling, budgeting, and operational execution, the EBIT margin can be improved in a lasting way without innovation capacity or market opportunities suffering as a result.

A strategy is only as good as its execution. Let us optimise your cost structure together: Strategy execution with scaleon

4. Lasting value through EBIT optimisation

A successful financial strategy should not only enable short-term cost reductions but also contribute to value creation and competitiveness over the long term. The agile cost efficiency approach goes beyond conventional cost-cutting measures and combines strategic resource use with operational efficiency.

Three central levers for a lasting improvement of the EBIT margin:

- Targeted resource allocation: Capital and budgets are directed where they create the greatest customer benefit and the highest strategic value. This keeps the company financially flexible without putting innovation potential at risk.

- Reduction of inefficient expenditure: Through continuous analysis of cost centres, unnecessary or oversized expenses can be eliminated systematically. Digital controlling tools and automated budget analyses help to identify savings potential at an early stage.

- Increase in operational efficiency: An agile corporate culture enables faster responses to market changes. Iterative optimisation processes and real-time reporting drive continuous improvements in the cost structure and contribute to a lasting increase in the EBIT margin.

5. Step by step toward better cost efficiency

To optimise costs efficiently and over the long term, companies should follow a structured approach. The following steps provide guidance:

- Baseline analysis:

- Cost optimisation begins with a detailed assessment of the current cost structure and budget utilisation.

- Identification of areas where high costs are associated with low value creation.

- Goal definition:

- Setting clear, measurable goals for improving the EBIT margin.

- Close coordination between the leadership level and operational teams to define strategic ambitions

- Introduction of agile methods:

- Iterative work cycles (sprints): rapid implementation and review of cost efficiency measures.

- OKRs (Objectives and Key Results): measurable goals that steer the implementation of efficiency improvements in a targeted manner. Learn more about OKR implementation

- Technological support:

- Development of automated dashboards and real-time reporting tools for transparent cost control.

- Use of analysis tools to visualise cost flows and conduct scenario analyses.

- Pilot projects and scaling:

- Starting with pilot projects in selected business units to test and adjust measures.

- Following successful implementation, a step-by-step roll-out across the entire company.

- Continuous improvement:

- Regular reviews and feedback loops to further develop measures dynamically.

- Promotion of a corporate culture that supports transparency and independently responsible cost management.

6. What is the best way to increase efficiency and reduce costs?

The key to successful cost reduction lies not in short-term savings measures but in a well-considered financial strategy that uses resources efficiently and enables strategic investment. Companies that focus exclusively on quick savings risk weakening their innovation capacity and competitiveness over the long term.

Lasting cost optimisation rests on three essential pillars:

- Strategic governance: Structured cost management that aligns savings with corporate growth goals.

- Dynamic budgeting: Flexible resource allocation ensures that investments are made precisely where they create the greatest value.

- Operational efficiency: Digital controlling tools and agile processes enable continuous review and adjustment of the cost structure.

Companies that master this balance between investment and cost control are more resilient in the face of market fluctuations and can improve their EBIT margin in a lasting way.

Strategic cost efficiency begins with the right planning. Discover how to develop a lasting strategy: Strategy development with scaleon